Equal Weighting: Genuine Diversification or Hidden Factor Risk?

Most broad equity indices are weighted according to market capitalisation. Under this approach, each company’s weight reflects its total market value, broadly calculated by multiplying its share price by the number of shares outstanding. A company worth £200 billion will therefore receive approximately twice the portfolio weight of a company worth £100 billion.

Throughout this article, the terms ‘market-capitalisation weighting’ and ‘value weighting’ are used interchangeably. Both describe a portfolio in which companies are weighted according to their total market value. In this context, ‘value weighting’ should not be confused with value investing, where companies are selected because they appear inexpensive relative to earnings, book value or other fundamental measures. Malladi and Fabozzi (2017), for example, use ‘value-weighted’ as another term for a conventional market-capitalisation-weighted portfolio.

An equal-weighted index follows a very different rule. Instead of allowing market values to determine the allocations, it gives every company the same weight. If an index contains 500 constituents, each company initially represents approximately 0.2% of the portfolio, irrespective of its economic size.

This sounds appealing and, indeed, Dai and Saito (2022) find that equal-weighted strategies tend to outperform their market-capitalisation-weighted counterparts before risk is considered.

Intuitively, equal weighting prevents a handful of large companies from dominating the portfolio and spreads capital more evenly across individual holdings. It is also often promoted as a systematic way of selling stocks after they have risen and buying them after they have fallen.

However, equal weighting does much more than reduce exposure to the largest companies. It materially changes the portfolio’s exposure to company size, value, profitability, liquidity and momentum. It also requires more trading and can cause the portfolio to behave very differently from the broad equity market.

The relevant question is therefore not simply whether equal weighting has produced higher historical returns. It is whether those returns represent a more efficient portfolio or compensation for accepting a different and potentially more aggressive collection of risks.

Why Market-Capitalisation Weighting Is the Default

The theoretical foundations of market-capitalisation weighting are commonly linked to the Capital Asset Pricing Model and the Efficient Market Hypothesis. In broad terms, market prices reflect the information, expectations and required returns of investors. A portfolio representing the whole market therefore provides a natural starting point for an investor who does not possess information that is already absent from prices (Malladi and Fabozzi 2017).

This does not mean that markets are always perfectly efficient or that every security is correctly priced. It means that departing from market weights represents an active decision. The investor must place more weight on some companies and less on others than the market collectively assigns to them.

Market-capitalisation weighting also has an important practical advantage. It is largely self-rebalancing.

When a company’s share price rises, its market value and index weight increase automatically. When its price falls, its weight decreases. A fund tracking the index does not ordinarily need to trade simply because prices have moved.

Equal weighting works differently. Price movements continually push each holding away from its target allocation. The fund must therefore rebalance periodically, selling companies that have grown beyond their equal weight and purchasing those that have fallen below it.

Market weighting is consequently not just a choice about which companies receive the largest allocations. It is also a relatively low-turnover method of allowing market prices to determine how the portfolio develops.

Equal Weighting Is Not a Neutral Portfolio

Equal weighting is sometimes treated as though it were a purer form of passive investing. Every company receives the same allocation, so the approach appears to avoid making judgements about which businesses deserve the greatest weight.

In reality, ignoring company size is itself an active judgement.

Suppose that the largest company in an index is worth 100 times more than one of its smaller constituents. A market-weighted portfolio recognises that difference through its allocations. An equal-weighted portfolio treats the two companies as equally important.

The result is a substantial transfer of capital away from the largest businesses and towards smaller companies. Equal weighting is therefore better understood as a systematic small-company strategy than as a neutral version of the market.

Dai and Saito (2022) examine eight different weighting methods and argue that approaches which do not maintain a close connection between prices and portfolio weights can create extreme and uncontrolled deviations from the market. Equal weighting is one of the methods they identify as producing greater turnover, higher costs and less predictable risk exposures.

The Structural Small-Company Tilt

The small-company exposure created by equal weighting is not incidental. It follows directly from the construction method.

In a market-capitalisation-weighted portfolio, the combined allocation to smaller companies remains relatively low because those companies account for a relatively small proportion of the market’s total value. In an equal-weighted portfolio, every small constituent receives the same allocation as the largest company.

As there are usually far more small companies than exceptionally large ones, smaller businesses can collectively occupy most of an equal-weighted portfolio.

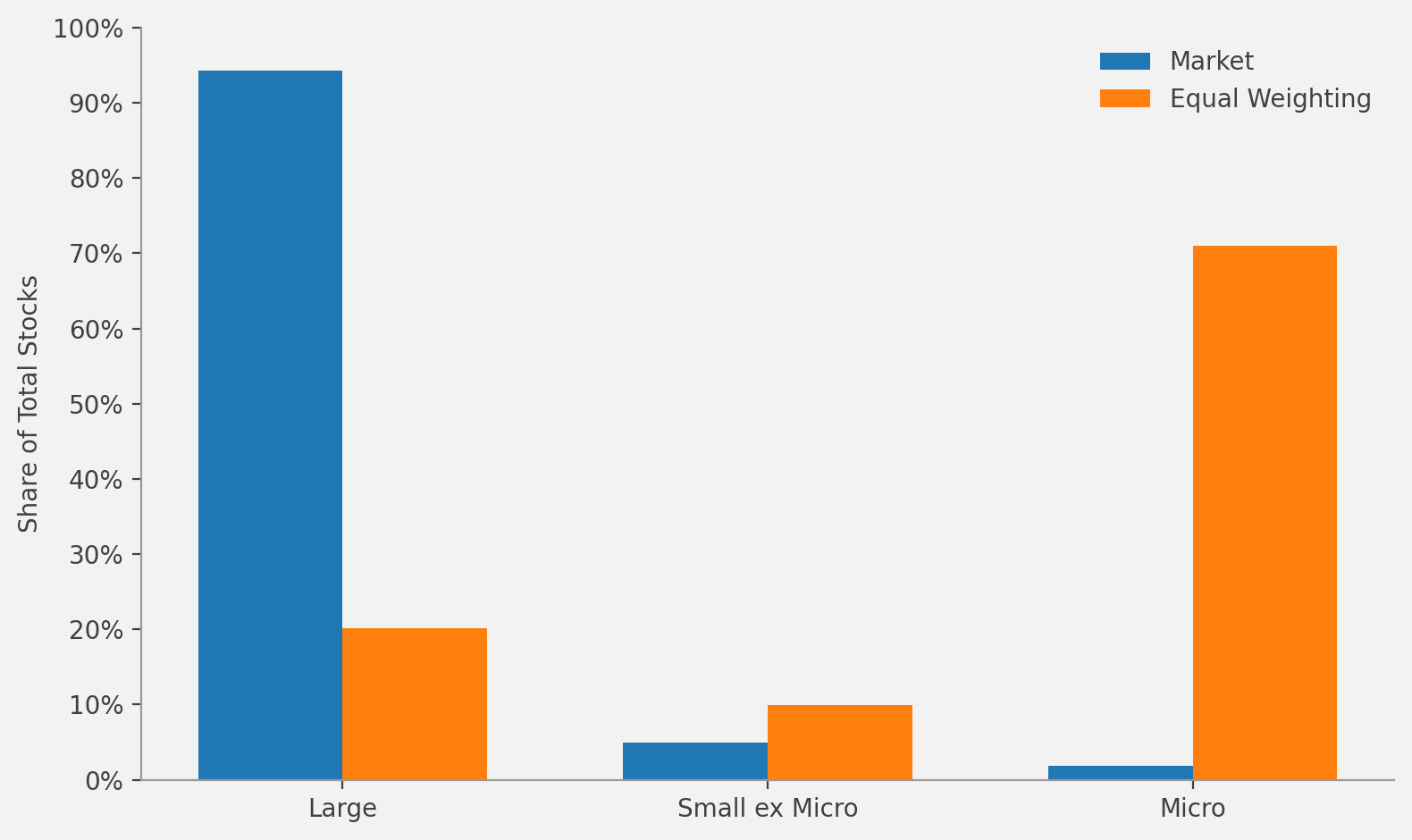

Dai and Saito (2022) find that approximately two-thirds of the assets in an equal-weighted all-cap US strategy are allocated to micro-cap stocks, even though micro-caps represent only a small proportion of the market’s total capitalisation. Their study covers US equities between 1974 and 2019.

This has important implications for how historical performance is interpreted. Small companies may offer higher expected returns than large companies, but they are also generally less established, less liquid and more vulnerable to financial distress.

Malladi and Fabozzi (2017) similarly show that equal weighting benefits when smaller companies outperform larger ones. Their theoretical model demonstrates that, following rebalancing, an equal-weighted portfolio produces a higher return when the smaller company subsequently performs better than the larger company.

An equal-weighted strategy may therefore outperform partly because it assumes more small-company risk. That is not the same as proving that the weighting rule itself creates a free or unexplained source of return.

Dai and Saito attempt to separate these effects by excluding micro-cap companies from the investable universe. Once this extreme size exposure is removed, the equal-weighted strategy’s estimated alpha relative to the market becomes statistically insignificant.

This suggests that much of the apparent advantage of equal weighting can be explained by its strong exposure to smaller companies (the size factor) rather than by equal weighting independently producing superior returns.

Figure 1. Size exposure within market-cap vs equal weighting strategies adapted from Dai et al., 2022. Approximately two thirds of equal weighting’s strategy is invested in micro-cap stocks.

Diversification Depends on More Than the Number of Holdings

Equal weighting unquestionably reduces concentration in the largest individual companies. This can be valuable for investors who are uncomfortable with an index becoming heavily dependent on a small number of dominant businesses.

However, company-level concentration is only one form of risk.

A portfolio can allocate 0.2% to each of 500 companies and still be concentrated in particular economic characteristics. For example, it may have unusually high exposure to:

Small and micro-cap companies;

Less liquid shares;

Businesses with relatively weak profitability;

Value stocks;

Particular sectors containing many smaller constituents; and

Companies whose prices have recently declined.

Equal weighting may therefore improve diversification by company name whilst reducing diversification across sources of risk.

It can also introduce substantial tracking error. Tracking error describes the extent to which a portfolio’s return differs from its benchmark. Because equal weighting departs considerably from the composition of the market, its performance can differ from a market-cap-weighted index for prolonged periods.

This is not necessarily undesirable. Any genuinely differentiated strategy will produce some tracking error. The important point is that investors should understand that an equal-weighted fund is not simply a better-balanced version of the same index. It is a different portfolio.

An Unintended Value Bias

Equal weighting also tends to create greater exposure to value stocks.

Dai and Saito (2022) find that approximately three-quarters of their equal-weighted portfolio is invested in value companies, compared with roughly half of the market portfolio. They also identify a greater allocation to companies with lower profitability.

This occurs partly because companies whose share prices have declined become smaller in market-capitalisation terms. In a market-weighted portfolio, their allocations fall naturally alongside their market values. An equal-weighted strategy instead purchases more shares at the next rebalance to restore their original weights.

That may prove profitable where markets have overreacted and the company subsequently recovers. However, a low valuation can also reflect genuine concerns about profitability, financial strength or future growth.

Equal weighting does not distinguish between a temporarily unpopular company and one experiencing a permanent deterioration in its business. It adds to both because the portfolio-construction rule requires it to do so.

A value tilt may increase expected returns over the long term, but it can also produce lengthy periods of underperformance. Investors experienced this during much of the 2010s, when growth companies materially outperformed value companies.

The issue is not that exposure to value stocks is inherently undesirable. It is that equal weighting introduces the exposure indirectly and with relatively little control over its size or quality.

Figure 2. Value exposure within market-cap vs equal weighting strategies adapted from Dai et al., 2022. Approximately four fifths of equal weighting’s strategy is invested in value stocks.

Selling Winners and Buying Losers

One of the most commonly cited advantages of equal weighting is its rebalancing discipline.

When one holding rises above its target weight, the strategy sells part of it. When another falls below its target, the strategy purchases more. This is often described as systematically ‘buying low and selling high’.

Malladi and Fabozzi (2017) identify rebalancing as an important source of equal weighting’s historical excess return. Using simulations and market data from 1926 to 2014, they conclude that equal-weighted portfolios have generally outperformed comparable value-weighted portfolios and that a meaningful part of this result is attributable to rebalancing.

However, the phrase ‘buy low and sell high’ can make the process sound more reliable than it is.

A company’s price may fall because investors have become excessively pessimistic. Alternatively, the price may fall because its competitive position, profitability or expected cash flows have genuinely weakened.

Likewise, a company whose share price has risen may not necessarily be overvalued. It may have developed a durable competitive advantage, increased its profitability or become more economically important.

Equal weighting does not assess whether a price movement is justified. It simply sells recent winners and adds to recent losers to maintain equal allocations.

This can be beneficial when prices reverse. It can be damaging when winners continue to outperform and struggling companies continue to decline.

Equal Weighting and Momentum

The repeated sale of recent winners also creates an implicit anti-momentum exposure.

Momentum refers to the historical tendency for stocks that have recently outperformed to continue outperforming over the following months, whilst recent underperformers may continue to struggle. Jegadeesh and Titman (1993) document significant positive returns from strategies that purchase recent winners and sell recent losers over holding periods of three to twelve months.

A momentum-aware investment strategy may delay selling a company that has performed strongly. It may also avoid immediately adding to a company whose price is falling.

Equal weighting generally does the reverse. At each rebalance, the strategy:

Reduces exposure to companies whose prices have risen;

Increases exposure to companies whose prices have fallen; and

Restores both groups to the same target weight.

This means that equal weighting systematically leans against recent price trends.

The effect should not be overstated. Equal-weighted portfolios do not represent pure short-momentum strategies, and their eventual performance depends on the interaction of numerous exposures. Nevertheless, their rebalancing rule can cause them to surrender some of the benefit associated with momentum.

A more sophisticated systematic portfolio can rebalance patiently, avoiding unnecessary purchases of securities with sharply negative momentum and delaying sales of strong recent performers.

Turnover Is Not Free

A market-capitalisation-weighted portfolio requires relatively little trading in response to price changes because its weights adjust automatically.

An equal-weighted portfolio must trade regularly to prevent its allocations from drifting. Dai and Saito (2022) estimate average annual turnover of approximately 32% for their equal-weighted strategy, compared with around 6% for the US market portfolio.

Higher turnover creates additional costs through:

Bid–ask spreads;

Brokerage and other transaction charges;

Taxes, where applicable;

Market impact; and

The operational cost of continually implementing trades.

These costs are particularly important because equal weighting directs so much capital towards smaller and less liquid companies.

Trading a large, highly liquid company is usually relatively straightforward. Buying or selling a meaningful position in a micro-cap company can be more difficult. The bid–ask spread may be wider, fewer shares may be available and a large trade may itself move the market price.

Backtests frequently assume that trades can be completed at or near the reported market price. In practice, the portfolio may receive a worse execution price, particularly when many investors attempt to trade the same less-liquid security.

Capacity and Liquidity Risk

The ability to implement equal weighting also depends on the size of the portfolio.

A small fund may be able to establish equal positions without materially affecting market prices. A large institutional portfolio could be required to hold substantial amounts of securities that trade only modest volumes each day.

Dai and Saito (2022) examine the proportion of each stock’s average daily trading volume that would need to be traded to maintain different weighting strategies. They find that portfolios which ignore market prices can require much greater participation in less-liquid securities.

This creates a capacity problem. As assets under management increase, the strategy may become harder and more expensive to implement.

It also creates a potential problem during stressed markets. If a fund must reduce its positions quickly, it may be unable to sell its smaller holdings without accepting sharply lower prices. An investment that appears liquid under ordinary conditions may become much less liquid when many investors attempt to exit simultaneously.

Illiquidity is therefore not merely an implementation inconvenience. It forms part of the risk exposure assumed by the investor.

Does Equal Weighting Produce Better Risk-Adjusted Returns?

Malladi and Fabozzi (2017) provide evidence that is broadly supportive of equal weighting.

Using simulations and historical US market data from 1926 to 2014, they find that equal-weighted portfolios generally produce higher returns than value-weighted portfolios. In their historical analysis, the equal-weighted portfolio produces approximately 1.03 percentage points more annual return and a higher overall Sharpe ratio.

The authors also conclude that, within their analysis, the additional return exceeds the greater transaction costs associated with higher turnover. They therefore argue that equal weighting can make economic sense even after estimated costs.

However, their results also demonstrate that the advantage is not consistent.

Equal-weighted portfolios generally experience higher volatility than their market-weighted counterparts. Malladi and Fabozzi define ‘excess risk’ as the standard deviation of the equal-weighted portfolio minus that of the equivalent value-weighted portfolio. This measure is positive in most of their simulations and historical comparisons.

The excess Sharpe ratio also varies through time. It is negative between 2009 and 2014, meaning that the additional return during this period is insufficient to compensate for the additional volatility.

This time variation is important. Equal weighting is particularly likely to perform well when smaller companies and value stocks outperform. When large growth companies lead the market, equal weighting can lag considerably.

Its historical success should therefore be understood in the context of its underlying factor exposures rather than treated as a permanent structural advantage.

Is Equal Weighting More Efficient?

Whether equal weighting is ‘better’ ultimately depends on what the investor is trying to achieve.

It may appeal to someone who:

Wants less dependence on the largest companies;

Accepts greater exposure to smaller businesses;

Is comfortable with substantial tracking error;

Believes that systematic rebalancing will add value;

Can tolerate long periods of relative underperformance; and

Understands the additional trading and liquidity risks.

Equal weighting is more compelling when it is presented simply as a safer or more diversified alternative to the market, but that would not be an accurate description of the strategy.

It reduces concentration in individual large companies, but it simultaneously increases exposure to small-company, value, liquidity and rebalancing risks. These risks may be rewarded over time, but they also may go through extended periods where they are not.

Investors seeking higher expected returns may be better served by a strategy that targets the desired sources of return directly.

For example, a purpose-built multifactor strategy could deliberately increase exposure to smaller or lower-priced value companies whilst:

Limiting exposure to micro-caps;

Favouring more profitable businesses;

Maintaining sector and security diversification;

Accounting for momentum;

Controlling turnover; and

Trading patiently to reduce market impact.

This provides greater control over which risks are being taken and how strongly they are represented.

Equal weighting combines several exposures through one simple rule. Its simplicity is attractive, but it is also its principal limitation.

Conclusion

Equal weighting should not be regarded as a neutral correction to market-capitalisation weighting. It is an active systematic strategy that produces a substantially different portfolio from the market.

By giving every company the same allocation, it moves capital away from the largest businesses and towards smaller, less liquid and often lower-priced companies. It also requires continual rebalancing, sells recent winners, purchases recent losers and can generate significant turnover and tracking error.

However, there is also credible evidence in its favour. Malladi and Fabozzi (2017) find that equal-weighted portfolios have historically delivered higher returns and, over their full sample, a modestly higher Sharpe ratio than value-weighted portfolios. They also identify rebalancing as an important source of the return advantage.

However, those higher returns arrive alongside higher volatility and are not consistent across all periods. Dai and Saito (2022) show that equal weighting can produce extreme small-company exposure, greater implementation costs and uncontrolled departures from the wider market.

Historical outperformance is therefore better understood as the result of a particular package of factor and implementation exposures rather than evidence that equal weighting offers a free improvement over market-capitalisation weighting.

For investors who consciously want small-company, value and rebalancing exposure, equal weighting may represent a reasonable systematic approach. For investors seeking broad, low-cost and relatively neutral participation in equity markets, market-capitalisation weighting remains the more straightforward starting point.

References

Dai, Wei, and Namiko Saito. 2022. ‘Weighting for the Right One: Weighting Scheme Design for Systematic Equity Portfolios.’ SSRN Electronic Journal. doi:10.2139/ssrn.4016481.

Jegadeesh, Narasimhan, and Sheridan Titman. 1993. ‘Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency.’ Journal of Finance 48 (1): 65–91. doi:10.1111/j.1540-6261.1993.tb04702.x.

Malladi, Rama K., and Frank J. Fabozzi. 2017. ‘Equal-Weighted Strategy: Why It Outperforms Value-Weighted Strategies? Theory and Evidence.’ Journal of Asset Management 18 (3): 188–208. doi:10.1057/s41260-016-0033-4.