Featured and Latest Posts

Managed Futures: What Are They All About?

Managed futures are strategies that use futures contracts to take long and short positions across markets such as equities, bonds, currencies and commodities. The best-known approach is trend following, where the strategy tries to participate in persistent price moves rather than predict the economy directly.

Their appeal is diversification. Unlike traditional equity and bond funds, managed futures are not dependent on markets rising and can potentially benefit from falling prices as well as rising prices. However, they are not portfolio insurance. They can struggle in choppy or trendless markets, and their ‘crisis alpha’ is not guaranteed. Used carefully, their role is best understood as a diversifying return stream rather than a replacement for equities or bonds.

Tracking Difference and Tracking Error

Tracking difference and tracking error are both used to judge how closely a fund follows its benchmark, but they answer different questions. Tracking difference tells you the actual return gap over a specific period: did the fund beat or lag the index, and by how much? For passive funds, this figure is often slightly negative because real-world funds face costs that an index does not, including ongoing charges, transaction costs and cash drag.

Tracking error, by contrast, tells you how variable that return gap was along the way. A fund can have a low tracking error whilst still consistently lagging the index by a small amount. Put simply, tracking difference is where the fund finished relative to the benchmark; tracking error is how smooth or erratic the journey was.

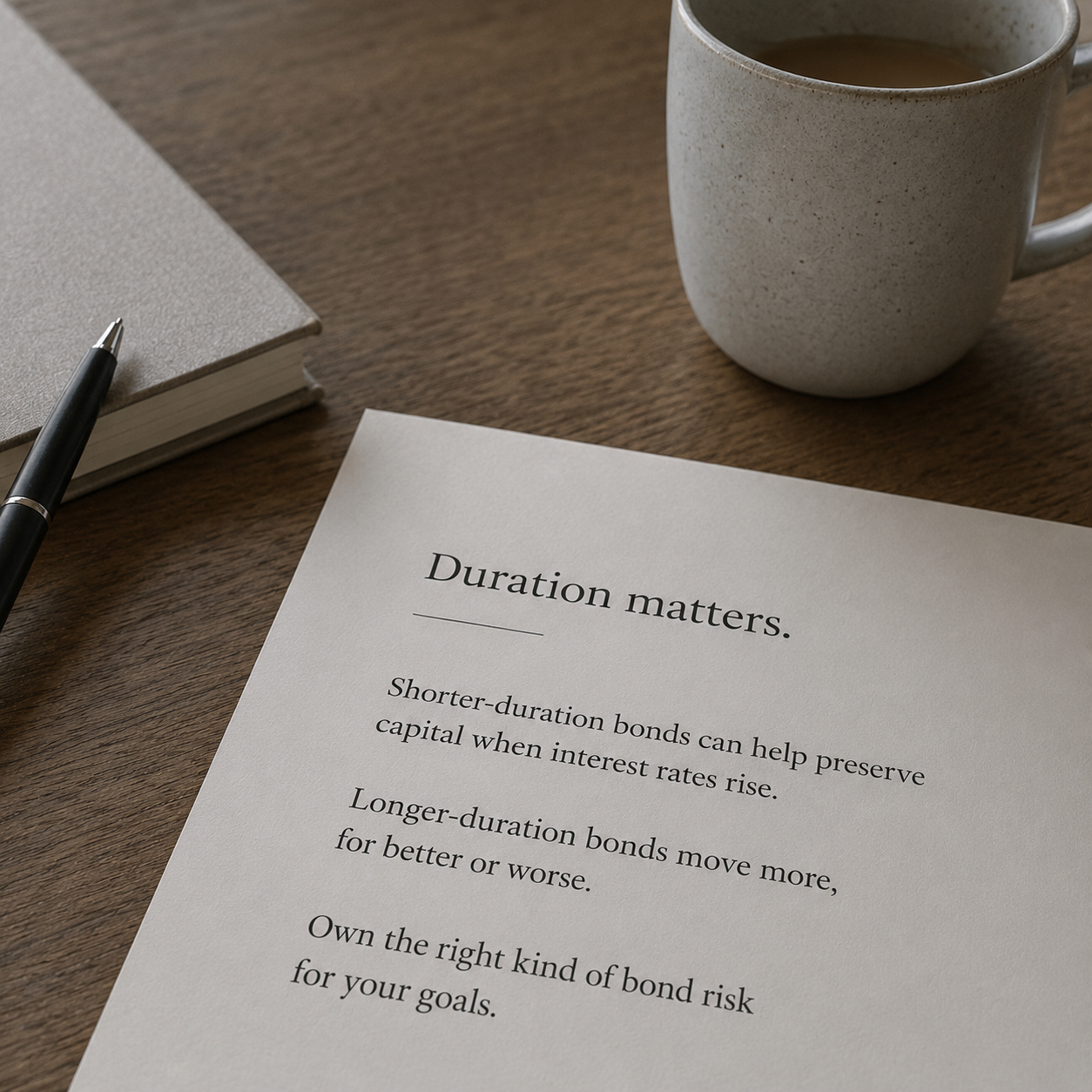

How Can a Bond Fund Fall by Over 50% in a One Year Period?

Bonds are often treated as the safe, defensive part of a portfolio, but that description can hide an important distinction. A short-duration government bond fund and a long-duration gilt fund are not simply different versions of the same thing; they can behave very differently when interest rates move. Duration is the key measure: the longer the duration, the more sensitive the bond’s price is to changes in yields.

The experience of long-dated gilts in 2022 showed this clearly. Rising yields led to large falls in long-duration bond funds, with losses that looked much closer to equity-market drawdowns than many investors would expect from ‘safe’ assets. This does not mean long-duration bonds are bad, but it does mean investors need to be clear about the role bonds are meant to play. For capital preservation, spending needs and portfolio stability, shorter-duration bonds may be better aligned with the job investors usually expect their defensive assets to do.

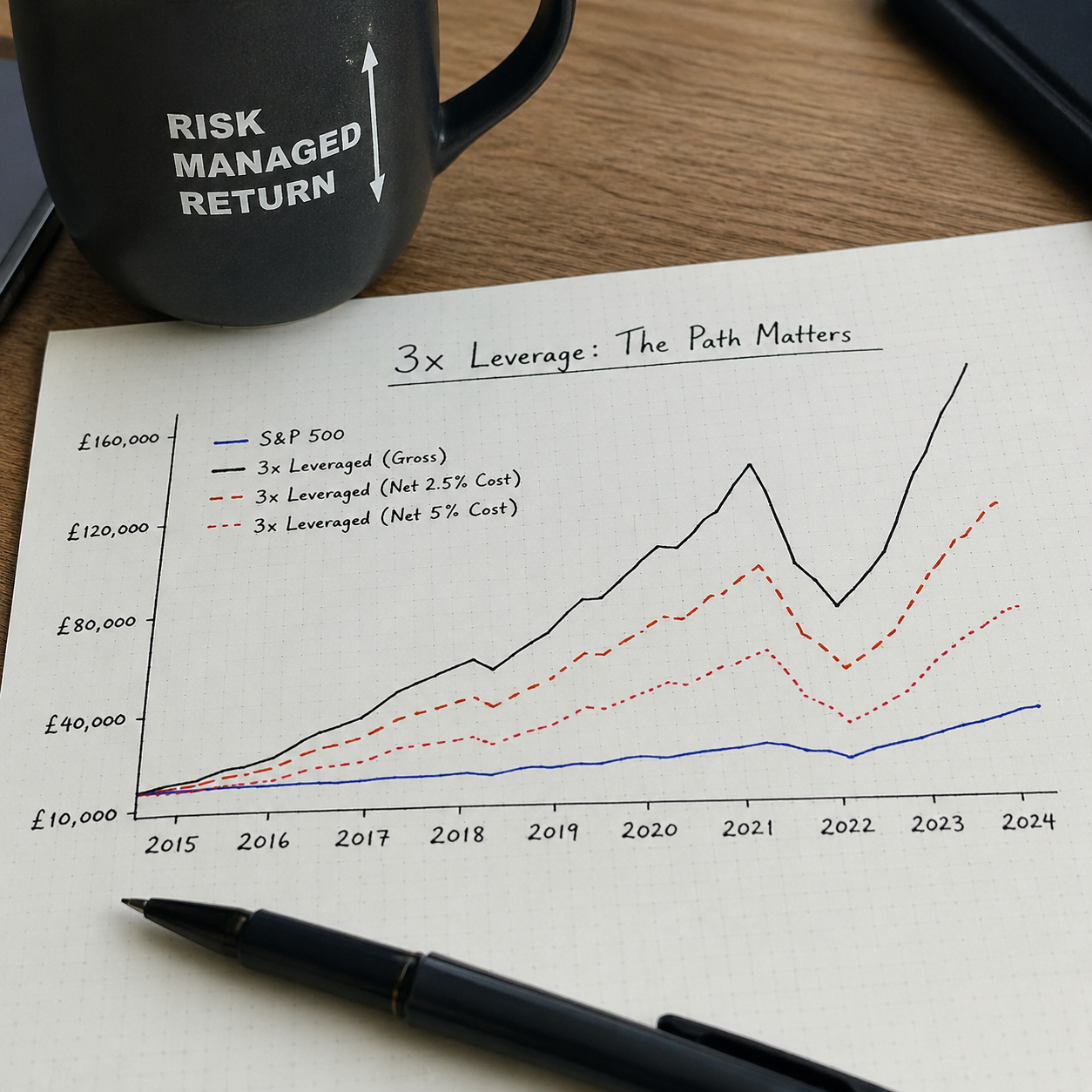

Are Complex Investment Strategies Harmful to Investors?

Complex investment strategies are not necessarily bad, but they often make risk harder to see and understand. A 3x leveraged S&P 500 strategy can look attractive in a strong decade, yet it is not simply ‘the S&P 500, but more of it’. It is a financed derivative position where gains, losses, costs and behavioural pressure are all magnified.

The real test is not whether equities rise over the long term, but whether the strategy can survive the period. Financing costs can materially reduce returns, drawdowns can become intolerable, and a bad decade can wipe out the investor before any recovery arrives. For most long-term investors, simplicity is not a weakness; it is often what allows them to stay invested.

Good financial decisions aren’t about predicting the future, they’re about following a sound process today.

In investing, outcomes are noisy. Short-term performance often reflects randomness, not skill. Yet fund managers continue to pitch five-year track records as if they prove anything. They don’t.

As Ken French puts it, a five-year chart ‘tells you nothing’. The real skill lies in filtering out the noise, evaluating strategy, incentives, costs, and behavioural fit.

Don’t chase what worked recently. Stick with what works reliably.