The ESG & Ethical Trade-off: Lower Returns for a Cleaner Conscience?

Over the past two decades, ESG (environmental, social, and governance) and ethical investing have moved from the margins of portfolio theory to the mainstream of financial markets. Fuelled by climate concerns, social justice movements, and regulatory scrutiny, sustainable investing has grown from a niche strategy to an industry staple. According to the Global Sustainable Investment Alliance (GSIA 2021), more than $35 trillion, over a third of global professionally managed assets, now claim to integrate ESG considerations.

But beneath the marketing gloss lies a fundamental set of tensions: Do ESG and ethical portfolios genuinely deliver better outcomes for society and the planet? Or do they merely make investors feel better about themselves, whilst imposing opportunity costs in the form of lower expected returns? Could it, in fact, be more effective to invest in ‘dirty’ but profitable companies and donate the excess returns to high-impact causes?

This article explores the core concepts, theoretical foundations, and practical trade-offs at the heart of sustainable investing.

1. Defining ESG, Ethical, and Sustainable Investing

The terminology around responsible investing is notoriously muddled. Whilst often used interchangeably, ESG, ethical, sustainable, and impact investing represent distinct (albeit overlapping) approaches:

ESG Investing involves incorporating environmental, social, and governance factors into investment analysis and decision-making. It does not necessarily exclude any companies or sectors but aims to manage material non-financial risks (Pedersen, Fitzgibbons, and Pomorski 2021).

Ethical Investing is based on moral or religious principles. Investors exclude companies or industries deemed incompatible with their values, such as fossil fuels, tobacco, gambling, or weapons, regardless of financial merit (Sparkes and Cowton 2004).

Sustainable Investing is an umbrella term that encompasses ESG, ethical, and impact strategies. It generally denotes an intent to align capital with long-term environmental and social sustainability.

Impact Investing goes further, aiming to generate measurable, intentional social or environmental outcomes, often alongside a concessionary financial return (Brest, Gilson, and Wolfson 2018).

Understanding these distinctions is critical because different motivations, risk management, moral alignment, or real-world impact, lead to different portfolio implications.

2. Why ESG and Ethical Portfolios Tend to Have Lower Expected Returns

The Asset Pricing Framework

In standard finance theory, expected returns are determined by risk and market demand. If a large cohort of investors refuses to hold certain stocks, those assets fall in price until their expected returns rise to compensate those willing to bear the associated risk, be it regulatory, reputational, or ethical (Heinkel, Kraus, and Zechner 2001). From a manager’s perspective, a higher cost of capital raises the hurdle rate a project must exceed to be considered worthwhile. This means that only projects with higher expected returns get funded, aligning the firm’s future cash flows with investor expectations for greater compensation.

This phenomenon leads to a ‘tilting premium’:

Firms in excluded industries, often termed ‘brown stocks’, have a higher cost of capital and thus offer higher expected returns to compensate for being shunned (Hong and Kacperczyk 2009).

ESG-compliant firms, conversely, attract capital inflows, leading to higher prices, a lower cost of capital and lower expected returns for investors.

This implies a fundamental trade-off: the more you align your portfolio with ethical or ESG preferences, the more you may sacrifice long-run returns (Pastor, Stambaugh, and Taylor 2021).

Behavioural and Transitional Counterarguments

Some ESG advocates argue that ESG integration improves returns by identifying firms better positioned for the future (Khan, Serafeim, and Yoon 2016). Whilst ESG may provide short-term performance boosts during periods of capital inflow, these effects are unlikely to persist. Once ESG becomes fully priced in, future returns should converge to below-market levels unless supported by fundamental risk exposure.

Pedersen, Fitzgibbons, and Pomorski (2021) mathematically formalise this trade-off through the concept of the ‘ESG-efficient frontier’, showing that investors face a spectrum between financial return and ESG alignment, analogous to risk-return trade-offs in traditional portfolio theory.

3. The Cost of Capital Channel and Real-Economy Impact

As we have shown above, from a corporate perspective, the cost of capital is the expected return demanded by investors. ESG firms enjoy lower costs of capital, making it easier to fund new projects. Brown firms, particularly those in fossil fuels or heavy industry, face a higher hurdle rate for investment, potentially deterring capital spending and accelerating their decline.

Thus, some argue that ESG investing exerts a real-economy effect by:

Raising the cost of capital for harmful industries

Lowering it for sustainable alternatives

Nudging corporate behaviour through capital allocation

However, the effectiveness of this mechanism depends on the extent to which capital constraints influence firm behaviour, a relationship that remains empirically ambiguous (Berk and van Binsbergen 2021).

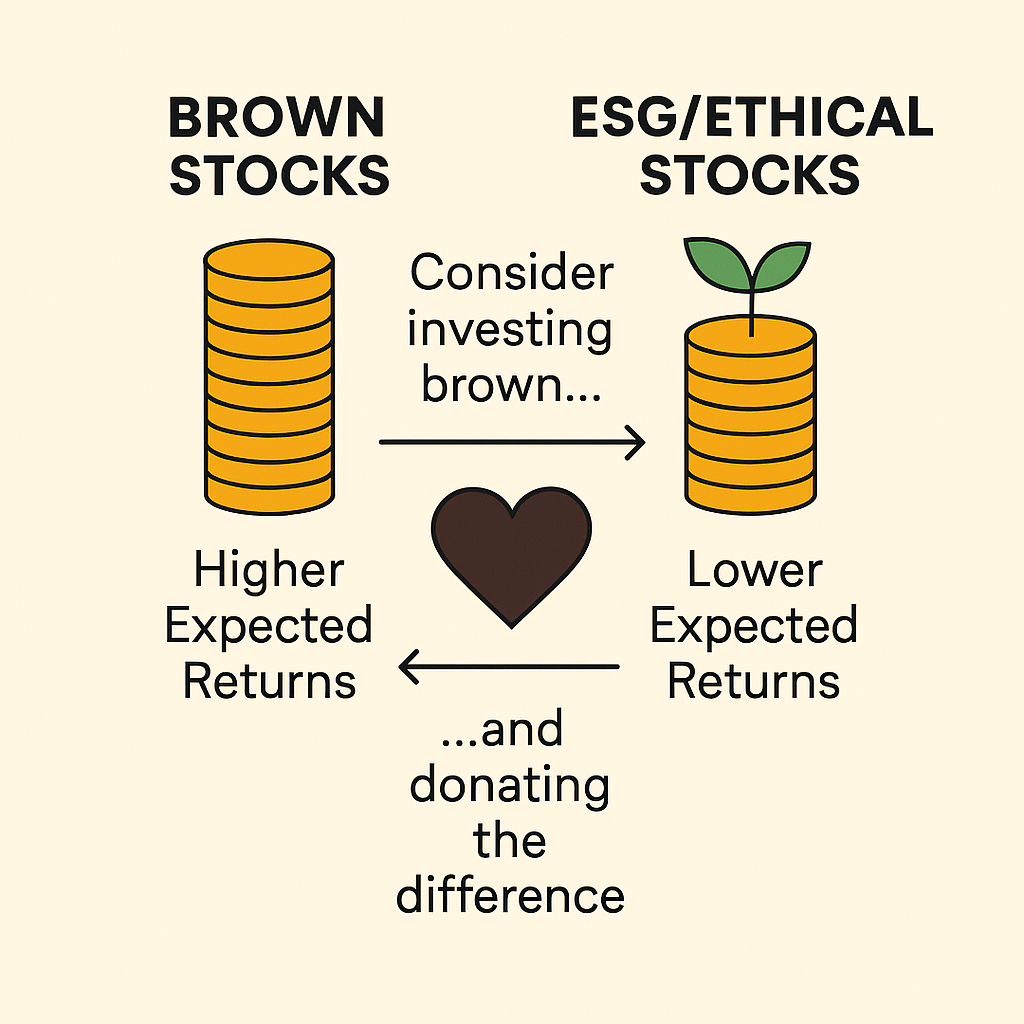

4. Why ‘Invest and Donate’ May Be the Superior Strategy

Whilst ESG investing may provide psychological alignment, it may not be the most effective way to improve the world. This is the central insight of the ‘invest and donate’ thesis:

Rather than excluding brown stocks, invest in them to earn higher expected returns and donate the difference to high-impact charities working on environmental or social issues.

This strategy is advocated for by Berk and van Binsbergen (2021), who argue that avoiding profitable brown firms does little to change their behaviour, whilst sacrificing capital that could otherwise be deployed for real change. They find that the impact of ESG exclusion on firms' cost of capital is economically small, implying limited real-world effects.

Asness (2017) frames the debate as one of virtue versus impact: are you trying to feel virtuous, or are you trying to maximise utility for society?

5. The Myth of ESG Alpha: Illusion, Misattribution, and Arbitrage

One of the most persistent and seductive claims in the sustainable investing movement is that ESG strategies not only align with one’s values but also outperform traditional investment approaches. This proposition has broad appeal: do well by doing good. Numerous fund managers, index providers, and ESG-labelled products assert that investors can achieve superior returns without sacrificing principles.

However, a growing body of empirical evidence suggests that most ESG outperformance is either an artefact of recent capital flows, misattributed factor exposures, or statistical sleight of hand. Once adjusted for these elements, the case for long-term ESG alpha becomes tenuous at best.

5.1 Short-Term ESG Outperformance: Driven by Inflows, Not Fundamentals

Between 2018 and 2021, many ESG-focused funds did outperform their non-ESG counterparts. This period coincided with:

A surge in investor demand for sustainable strategies

Regulatory and disclosure mandates (e.g. SFDR in Europe)

Broad underperformance of the energy and traditional industrial sectors

A rally in large-cap, high-profitability firms; often overrepresented in ESG portfolios

As capital flooded into ESG-labelled funds, demand drove up valuations, creating a momentum-like effect. Pastor, Stambaugh, and Taylor (2021) describe this as ESG ‘tilting’, investors moving en masse into ESG stocks, compressing expected returns but temporarily boosting realised ones. The result: backward-looking returns looked excellent, but forward-looking expectations deteriorated.

This phenomenon is not new. Flows into any investment style can produce transient outperformance. Once the style becomes saturated or overvalued, future returns revert. ESG may have simply experienced its version of a popular style cycle.

5.2 The Factor Mirage: Profitability and Quality Drive ESG Returns

ESG performance often mirrors exposures to known equity factors. For instance:

Profitability: ESG portfolios tend to favour companies with strong operating margins, high return on assets, and efficient capital allocation. These traits directly overlap with the profitability factor in the Fama-French five-factor model (Fama and French 2015).

Quality: Many ESG scoring systems reward stable earnings, low leverage, and sound corporate governance; traits that map closely to the quality factor as formalised by Asness, Frazzini, and Pedersen (2019).

Low Volatility: ESG portfolios frequently underweight controversial or cyclical sectors, unintentionally tilting towards lower-beta or more stable stocks.

Momentum: Popular ESG holdings often display strong recent performance, leading to incidental exposure to momentum.

➤ When these exposures are accounted for, the residual ESG alpha disappears. ESG funds are not beating the market because of superior sustainability insights; they are often just repackaged multi-factor strategies.

Blitz and Fabozzi (2017) find that ESG-labelled strategies do not generate positive alpha after adjusting for factor exposures, particularly profitability and low risk. The illusion of alpha vanishes under proper risk decomposition.

5.3 Inconsistent Ratings: The Problem of ESG Noise

A further complication is the low agreement among ESG rating providers. ESG ratings for the same firm can differ dramatically across providers due to differences in:

Indicator selection

Measurement methodology

Weighting of sub-categories

Materiality frameworks

Berg, Kölbel, and Rigobon (2022) term this ‘aggregate confusion’, showing that ESG scores have average correlations of just 0.61, far lower than credit ratings. The correlation between market-cap-weighted indices from different providers, such as the S&P 500 (S&P Dow Jones), MSCI USA, and FTSE USA, is typically very high, often exceeding 0.99 over long-term horizons. This lack of consistency regarding ESG ratings reduces confidence in ESG portfolio construction and challenges claims of skill-based alpha.

If ESG itself lacks a coherent and consistent definition, it becomes difficult to argue that ESG outperformance is anything more than a fortunate alignment with other quantifiable traits.

5.4 Greenwashing and Marketing Arbitrage

In the rush to capture capital inflows, many asset managers have rebranded conventional strategies as ESG, often with minimal underlying change. This practice, greenwashing, has become widespread and difficult to monitor.

Green, Jame, and Markov (2017) find that adding ESG-related terms to fund names significantly increases investor capital inflows, regardless of actual sustainability performance. This suggests a strong behavioural preference among investors, which firms exploit through marketing rather than substance.

This branding arbitrage raises questions about how much of ESG fund performance is attributable to genuine ESG insights versus momentum from investor demand.

5.5 The Saturation Problem: Crowding and Return Compression

As ESG investing grows, it risks becoming a crowded trade. Capital has poured into a relatively narrow group of ESG-compliant companies, bidding up valuations and compressing expected returns.

Pastor, Stambaugh, and Taylor (2021) argue that as ESG becomes more universally adopted, its efficacy diminishes. Early adopters may have benefited from mispricing or inefficiencies, but widespread uptake arbitrages away these benefits.

➤ In the long run, ESG becomes a negative expected return tilt unless investors are explicitly willing to sacrifice return for personal or societal utility.

5.6 Summary: An Elegant Narrative, But a Fragile Foundation

The idea that ESG investing systematically outperforms the market is comforting, but it often rests on unstable empirical ground. Most of the observed outperformance stems from:

Short-term capital inflows

Profitability and quality factor tilts

Sector biases

Inconsistent definitions

Marketing opportunism

A rigorous, factor-aware analysis shows that ESG alpha is largely an illusion. This doesn’t invalidate ESG investing but it does require honest acknowledgement of what drives returns.

Investors must ask: are you pursuing impact, alignment, or outperformance? Only one of those goals is realistically achievable in the long run and it’s rarely all three (Hale 2023).

6. What Should an Evidence-Based Investor Do?

An investor with evidence-based discipline should ask:

What are my goals: personal alignment, financial return, or real-world impact?

Am I willing to accept lower returns for the sake of ethical consistency?

Would donating to effective charities be a better way to make a difference?

If impact is the goal, targeted philanthropy combined with diversified investing may be superior to ESG screening. If values alignment is critical, then an ESG or ethical fund may offer peace of mind, even if at a cost.

Conclusion

ESG and ethical investing appeal to investors seeking to align their capital with their values. However, by altering capital flows and valuations, they also affect asset prices and expected returns. Ethical portfolios may yield lower long-term returns, whilst brown stocks, shunned by many, offer a return premium for those willing to bear reputational or normative discomfort.

Investors should be wary of claims that ESG investing offers superior returns with no cost. Instead, a more honest conversation recognises the trade-offs between return, values, and impact and the possibility that ‘doing well by doing good’ may come at a price.

References

Asness, Clifford. 2017. ‘Virtue Is Its Own Reward: Or, One Man’s Ceiling Is Another Man’s Floor’. AQR Blog, 10 October 2017. https://www.aqr.com

Berg, Florian, Julian F. Kölbel, and Roberto Rigobon. 2022. ‘Aggregate Confusion: The Divergence of ESG Ratings’. Review of Finance 26 (6): 1315–44. https://doi.org/10.1093/rof/rfac033

Berk, Jonathan B., and Jules H. van Binsbergen. 2021. ‘The Impact of Impact Investing’. Journal of Financial Economics 142 (2): 572–87. https://doi.org/10.1016/j.jfineco.2021.05.031

Brest, Paul, Ronald J. Gilson, and Mark A. Wolfson. 2018. ‘Maximizing Social Returns through ESG Investing’. Stanford Social Innovation Review, Winter 2018.

Global Sustainable Investment Alliance (GSIA). 2021. Global Sustainable Investment Review 2020. https://www.gsi-alliance.org

Green, T. Clifton, Russell E. Jame, and Stanimir Markov. 2017. ‘The Impact of Socially Responsible Mutual Fund Names on Investor Flows’. Journal of Financial Economics 124 (3): 605–26.

Hale, T. 2023. Smarter Investing: Simpler Decisions for Better Results. 4th ed. FT Publishing International.

Heinkel, Robert, Alan Kraus, and Josef Zechner. 2001. ‘The Effect of Green Investment on Corporate Behavior’. Journal of Financial and Quantitative Analysis 36 (4): 431–49. https://doi.org/10.2307/2676219

Hong, Harrison, and Marcin Kacperczyk. 2009. ‘The Price of Sin: The Effects of Social Norms on Markets’. Journal of Financial Economics 93 (1): 15–36. https://doi.org/10.1016/j.jfineco.2008.09.001

Khan, Mozaffar N., George Serafeim, and Aaron Yoon. 2016. ‘Corporate Sustainability: First Evidence on Materiality’. The Accounting Review 91 (6): 1697–1724.

Pastor, Lubos, Robert F. Stambaugh, and Lucian A. Taylor. 2021. ‘Dissecting Green Returns’. Journal of Financial Economics 142 (2): 1037–54. https://doi.org/10.1016/j.jfineco.2021.06.014

Pedersen, Lasse Heje, Shaun Fitzgibbons, and Lukasz Pomorski. 2021. ‘Responsible Investing: The ESG-Efficient Frontier’. Journal of Financial Economics 142 (2): 572–97. https://doi.org/10.1016/j.jfineco.2021.01.014

Sparkes, Russell, and Christopher J. Cowton. 2004. ‘The Maturing of Socially Responsible Investment: A Review of the Developing Link with Corporate Social Responsibility’. Journal of Business Ethics 52 (1): 45–57. https://doi.org/10.1023/B:BUSI.0000033106.43260.99