Understanding Convertible Bonds: A Hybrid Between Debt and Equity

Convertible bonds are a fascinating financial instrument that straddle the line between fixed income and equities. They offer investors a unique combination of downside protection and upside potential, while also serving as a flexible financing tool for companies. In this post, we’ll explore what convertible bonds are, how they work, and why both investors and issuers find them attractive.

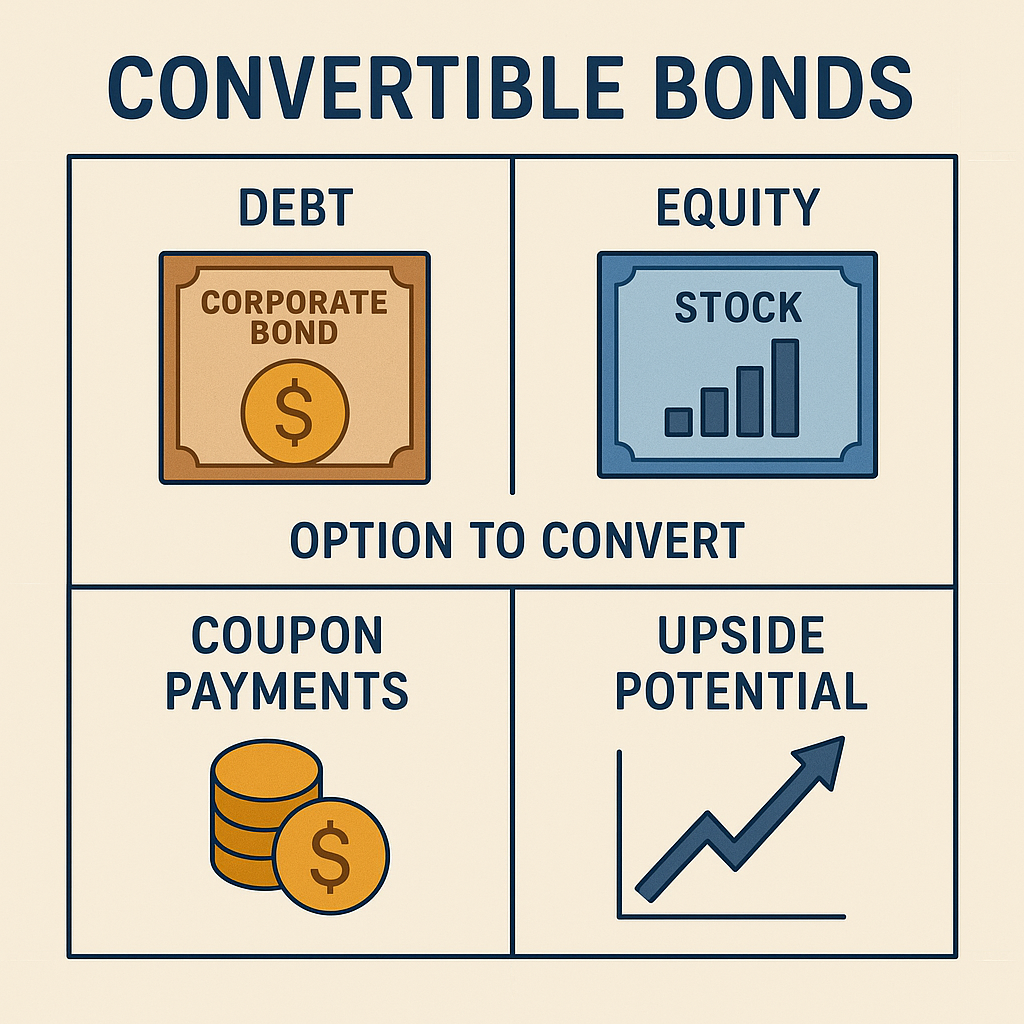

What Are Convertible Bonds?

A convertible bond is a type of corporate bond that includes an embedded option allowing the bondholder to convert the bond into a predetermined number of shares of the issuing company’s stock. This option is usually exercisable at the discretion of the investor, although certain types may convert automatically under specific conditions.

In essence, convertible bonds allow investors to participate in the potential upside of a company’s equity while retaining the income and capital preservation features of a traditional bond (Fabozzi 2021).

Key Features

Like conventional bonds, convertibles pay interest (known as coupon payments) and return the principal at maturity, unless the bondholder opts to convert the bond into equity. However, there are several distinct features that set them apart:

Coupon payments: Typically lower than non-convertible corporate bonds due to the added value of the conversion option.

Conversion ratio: The number of shares an investor receives upon conversion.

Conversion price: The effective price per share when the bond is converted, derived from the bond’s face value and conversion ratio.

Optionality: The investor holds the right, but not the obligation, to convert.

These features give convertible bonds a dual character: they behave like bonds when stock prices are low, and like equities when stock prices rise.

Why Companies Issue Them

From the issuer’s perspective, convertible bonds are an attractive alternative to traditional equity or debt issuance. The primary benefits include:

Lower borrowing costs: Firms can offer lower interest rates than standard bonds because investors are compensated with potential equity upside.

Deferred dilution: Conversion to shares occurs only if the bondholder exercises the option, delaying the dilution of existing shareholders.

Access to a broader investor base: Convertibles appeal to both income-oriented and growth-focused investors.

Moreover, issuing convertible bonds may signal to the market that the company has strong future growth expectations (Brealey, Myers, and Allen 2020).

Why Investors Like Them

Convertible bonds offer a rare combination of features that attract a wide range of investors:

Downside protection: If the company’s stock underperforms, the investor still receives interest payments and repayment of principal.

Equity upside: If the company’s share price rises, the conversion option becomes valuable, allowing investors to benefit from capital appreciation.

Portfolio diversification: Convertibles exhibit hybrid characteristics, making them less correlated with traditional equities or bonds.

This asymmetric payoff structure is especially attractive in volatile markets or uncertain economic conditions (Tuckman and Serrat 2012).

Risks to Consider

Despite their appeal, convertible bonds come with several risks:

Interest rate risk: Like all bonds, their prices may decline if interest rates rise.

Credit risk: The financial health of the issuer can impact the ability to meet coupon and principal payments.

Equity risk: If the stock price remains below the conversion price, the conversion option may never be exercised, diminishing the bond’s overall return.

Investors must carefully evaluate the creditworthiness of the issuer and the likelihood of the equity price reaching conversion levels.

Types of Convertible Bonds

There are several variations of convertible bonds, including:

Vanilla convertibles: Standard bonds with a straightforward conversion option.

Mandatory convertibles: Automatically convert to equity at maturity, regardless of share price.

Reverse convertibles: Allow the issuer to repay in shares rather than cash, often in exchange for higher coupon payments.

Each type has its own risk–return profile and is suited to different investment strategies.

A Simple Example

Suppose you purchase a convertible bond with a face value of £1,000, a conversion ratio of 20, and therefore a conversion price of £50 (£1,000 ÷ 20). If the company’s share price rises to £60, you can convert the bond and effectively acquire shares at a discount, locking in a gain.

Conversely, if the share price stays below £50, you can hold the bond to maturity and collect the interest and principal payments.

Conclusion

Convertible bonds are a versatile and dynamic asset class that can play a strategic role in both corporate finance and portfolio construction. Their hybrid nature makes them an appealing choice for those seeking a balance between risk and reward.

For investors, they offer the rare chance to hedge downside while still enjoying equity-like gains. For companies, they represent a lower-cost, flexible financing tool that defers dilution. As always, careful analysis is required to assess their suitability in a given context.

References

Brealey, Richard A., Stewart C. Myers, and Franklin Allen. 2020. Principles of Corporate Finance. 13th ed. New York: McGraw-Hill Education.

Fabozzi, Frank J. 2021. Bond Markets, Analysis and Strategies. 10th ed. Boston: Pearson.

Tuckman, Bruce, and Angel Serrat. 2012. Fixed Income Securities: Tools for Today's Markets. 3rd ed. Hoboken, NJ: Wiley.