Featured and Latest Posts

MPS, Multi-Asset Funds and DFMs: What Is the Difference?

Model portfolio services, multi-asset funds and discretionary fund managers are often discussed as though they are interchangeable. In reality, they describe different parts of the investment process. A discretionary fund manager makes investment decisions, an MPS applies a centrally managed portfolio across individual client accounts, and a multi-asset fund combines several asset classes within a single pooled investment.

Although each approach can provide a professionally managed and diversified portfolio, their structure affects how investments are owned, rebalanced, taxed and transferred. Understanding these differences can help investors and advisers assess which solution offers the right balance of transparency, simplicity, flexibility and value.

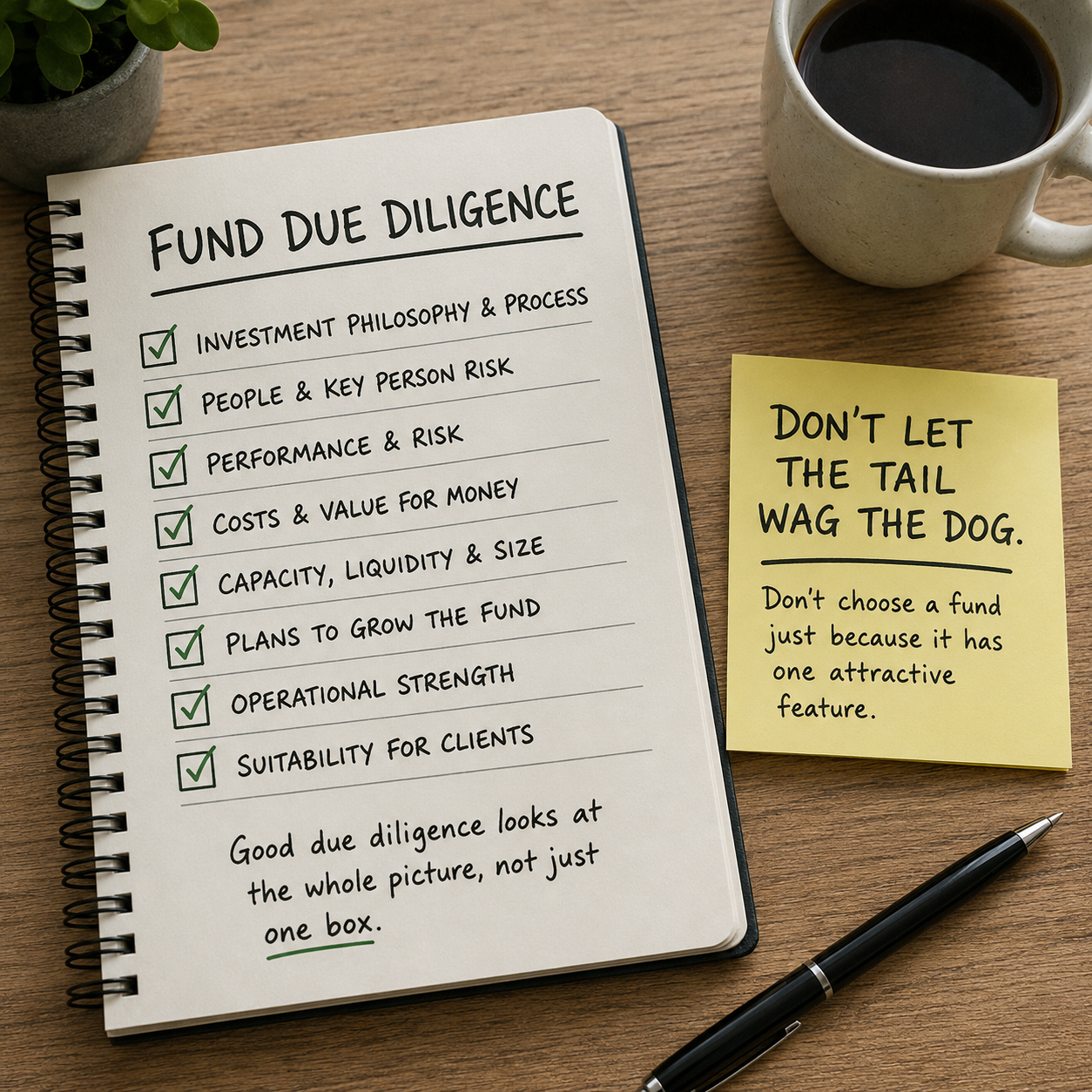

What Due Diligence Should an IFA Complete Before Adding a Fund to a Client Portfolio?

Fund due diligence is not about chasing recent performance. It is about understanding what a fund is designed to do, how it generates returns, who is responsible for it and what could go wrong. For an adviser, a robust process should consider philosophy, people, costs, liquidity, operational strength and client suitability, whilst documenting the reasons for selection and monitoring whether the original case remains valid over time.

Differences between the Most Prominent Index Families

A global equity tracker portfolio sounds simple: buy the developed world, add emerging markets, and you have covered most of the investable equity market. But the words ‘developed’ and ‘emerging’ do not mean exactly the same thing to every index provider. South Korea, Poland, Peru and Vietnam can sit in different places depending on whether the fund tracks MSCI, FTSE Russell, S&P DJI, Solactive or STOXX. For investors combining separate developed and emerging markets funds, that can create accidental gaps, overlaps and meaningful tracking error.

Managed Futures: What Are They All About?

Managed futures are strategies that use futures contracts to take long and short positions across markets such as equities, bonds, currencies and commodities. The best-known approach is trend following, where the strategy tries to participate in persistent price moves rather than predict the economy directly.

Their appeal is diversification. Unlike traditional equity and bond funds, managed futures are not dependent on markets rising and can potentially benefit from falling prices as well as rising prices. However, they are not portfolio insurance. They can struggle in choppy or trendless markets, and their ‘crisis alpha’ is not guaranteed. Used carefully, their role is best understood as a diversifying return stream rather than a replacement for equities or bonds.

Good financial decisions aren’t about predicting the future, they’re about following a sound process today.

In investing, outcomes are noisy. Short-term performance often reflects randomness, not skill. Yet fund managers continue to pitch five-year track records as if they prove anything. They don’t.

As Ken French puts it, a five-year chart ‘tells you nothing’. The real skill lies in filtering out the noise, evaluating strategy, incentives, costs, and behavioural fit.

Don’t chase what worked recently. Stick with what works reliably.