Featured and Latest Posts

Sharpe’s Arithmetic, Revisited: When ‘Average Active’ Might Beat ‘Average Passive’ Before Costs

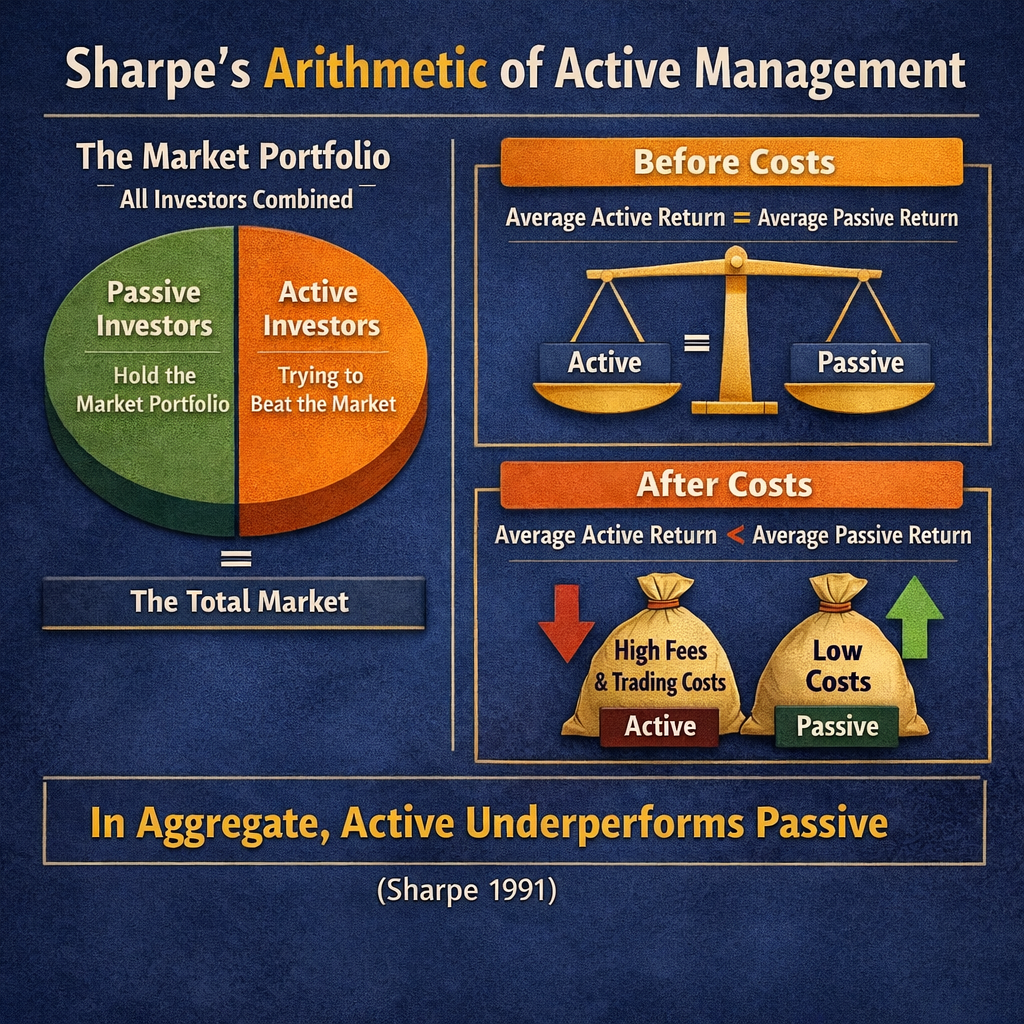

Sharpe’s ‘Arithmetic of Active Management’ is powerful because it is an accounting identity, not a claim about skill. If passive investors hold the market portfolio, then everyone else, collectively, must hold the same market portfolio too. That means, before costs, the average actively managed pound must earn the same return as the average passively managed pound. After costs, active underperforms in aggregate because it bears higher fees, turnover, and trading frictions.

The wrinkle is that the market portfolio is not static, and passive implementation is not continuous. Corporate actions reshape the investable set, whilst index trackers rebalance on rules and schedules, creating brief mismatches with the ‘instantaneous’ market. In that more realistic setting, average active can slightly outperform average passive before costs by intermediating those flows, without any special forecasting skill. But competition and costs still mean the core practical conclusion remains: passive tends to win after fees.

The Main Components of Bond Returns: Carry, Roll-down, and the Yield-curve Surprise

Bond returns can look deceptively simple: you lend money to a government or company, collect coupons, and get your principal back at maturity. The surprise is that, over short periods, even ‘safe’ bonds can fall sharply in value whilst still paying those coupons. That is not a glitch, it is just the market repricing what interest rates should be, and bond prices adjusting immediately.

A helpful way to think about it is that a bond’s return has three moving parts: what you get paid for holding it (carry), what you might gain simply because time passes on a normally upwards-sloping yield curve (roll-down), and the unpredictable bit (the yield-curve surprise). Carry and roll-down are the ‘expected’ components implied by today’s pricing. The surprise is ‘what the yield curve actually does’, and it can easily overwhelm the first two when interest rates change quickly.

Profitability and Investment Premia: What Fama–French’s ‘Quality’ Factors Mean for Investors

The Capital Asset Pricing Model (CAPM) assumes that a stock’s expected return is explained entirely by its sensitivity to the market portfolio: one factor, one beta. Yet in practice, the CAPM leaves much unexplained. Fama and French (1993) formalised these findings in their three-factor model, adding size (SMB) and value (HML) to the market factor.

Even then, further anomalies persisted. Portfolios sorted by profitability and investment intensity were not explained by the three-factor model. Fama and French (2015) expanded the framework to five factors, adding profitability (RMW—robust minus weak) and investment (CMA—conservative minus aggressive). This version explains the cross-section of returns more effectively, showing that much of what was previously attributed to value is better captured by profitability and investment.

For investors, RMW rewards exposure to firms with sustainable earnings, whilst CMA rewards avoiding those that pursue growth too aggressively. Profitability has been a consistent and defensive premium; investment more cyclical but valuable in filtering out overpriced growth.

The Size Premium Myth? Why Small May Need Friends

The so-called ‘size premium’, the idea that small companies reliably beat large ones, has always sounded intuitive. Smaller firms are riskier, less liquid, and harder to hold, so they should deliver higher returns. Yet the evidence is far from clear. Long-term data show bursts of small-cap outperformance, but these gains are patchy, fragile, and often vanish once you adjust for higher market betas. What really drives results is the company type: small-cap value and high-quality firms have consistently delivered, whilst small-cap growth has been persistently weak. The charts in this post make it plain. Size on its own is not a premium, but paired with value and profitability it remains a powerful portfolio building block.

Good financial decisions aren’t about predicting the future, they’re about following a sound process today.

In investing, outcomes are noisy. Short-term performance often reflects randomness, not skill. Yet fund managers continue to pitch five-year track records as if they prove anything. They don’t.

As Ken French puts it, a five-year chart ‘tells you nothing’. The real skill lies in filtering out the noise, evaluating strategy, incentives, costs, and behavioural fit.

Don’t chase what worked recently. Stick with what works reliably.